Improving the quality of life of low-income populations in Honduras, El Salvador, Panama and the Dominican Republic

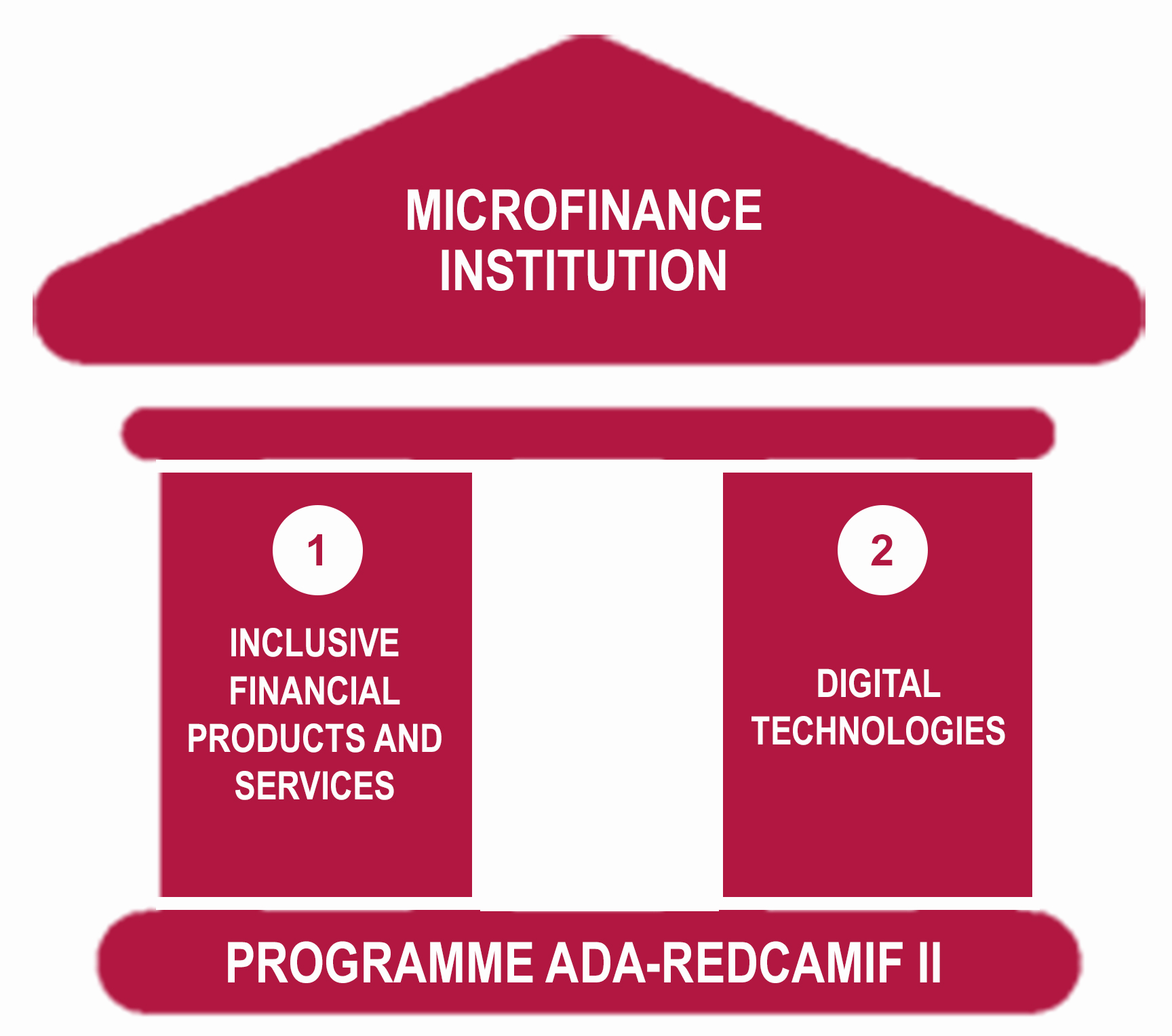

The ADA-REDCAMIF II programme (2018-2021) entitled "Strengthening the social added value of microfinance" aims at improving the quality of life of low-income populations in Central America and the Dominican Republic by providing access to responsible and inclusive financial services. To this end, the program supports microfinance institutions (MFIs) in:

The ADA-REDCAMIF II programme (2018-2021) entitled "Strengthening the social added value of microfinance" aims at improving the quality of life of low-income populations in Central America and the Dominican Republic by providing access to responsible and inclusive financial services. To this end, the program supports microfinance institutions (MFIs) in:

- PILLAR 1 - Developing inclusive financial products and services: 19 MFIs received methodological and / or financial support through 22 projects to design new financial products or services, with added social value (more than one MFI was supported in several projects);

- PILLAR 2 - Using digital technologies to improve operations: 17 MFIs received support through 17 projects to implement digital solutions..

In total, 31 MFIs were supported through 39 projects in 7 countries in which the National Networks affiliated to REDCAMIF are represented - Guatemala, El Salvador, Honduras, Nicaragua, Costa Rica, Panama and the Dominican Republic. Every month, learn about key program projects.

PILLAR 1 - Developing inclusive financial products and services

PADECOMSM IN SALVADOR PROMOTES FINANCING FOR THE REDUCTION OF THE VULNERABILITY OF RURAL PRODUCERS

PADECOMSM is an organization with an important presence in the rural areas of El Salvador. Its mission emphasizes the provision of inclusive financial products and services with social and environmental responsibility. As of December 30 2020, it had 8,971 customers, 78% of which are rural. It focuses on supporting financing for farmers in El Salvador’s eastern region, where production consists mainly of staple grains, coffee, vegetables and small livestock. These sectors are the most vulnerable to the effects of climate change exposing them to extreme periods of drought that affect production and impact household income and the food security itself.

This is why PADECOMSM decided to promote initiatives contributing to the increase of resilience and the reduction of vulnerability among rural producers. To this end, it implemented a pilot for the adoption of a holistic green approach including a transformation in clients' farms and the incorporation of the green concept in the institution. The pilot project included three areas:

- Financial product design: it includes interest rate as an incentive, with a product family approach covering five end uses: eco-homes, sustainable businesses, sustainable agriculture, sustainable livestock farming and sustainable beekeeping. To date, 54 clients have been financed for a variety of practices and technologies including: efficient water management, implementation of new and improved crop varieties, and crop diversification, among others.

- Environmental education for clients: an environmental curriculum was designed with clients in mind, including both adoption of environmental practices in their production systems and the introduction of efficient productive technologies, such as education and awareness about issues related to climate change and the sustainable use of natural resources available in farms.

- Design of an environmental policy within the organization: it is already in use and includes positive discrimination criteria to avoid the financing of practices or technologies harmful to ecosystems and human health. The policy also includes a policy of saving, recycling and reducing energy-related expenses such as stationery, among others, and carrying out annual activities seeking to raise awareness among customers and collaborators such as delivering fruit and timber trees, celebrating the World Enviroment Day, the Day of the Tree in the institution

CREDICAMPO IN SALVADOR OFFERS AN EXTENSIVE PAYMENT NETWORK TO ITS CUSTOMERS

CREDICAMPO has most of its portfolio concentrated in rural areas of El Salvador, where mobilization, distance, and health and physical safety are key issues affecting client repayment performance. With this in mind, the institution decided to implement digital initiatives in 2019 to expand and streamline its payment network to make it easier for customers to carry out payments by bringing service points closer to them.

A year later a survey was conducted among clients to know about their pain points. Among the main improvements were the setting-up a web service and changes made to the supplier system, now allowing a direct real-time interaction between both systems so that payments are applied the same day and customers can check their account balance to date in a receipt.

CREDICAMPO’s Payment Network has national coverage through more than 400 24/7 service points, guaranteeing that payments made through its collections agents (pharmacies, gas stations, and supermarkets, among others) are reliable, transparent and safe, as the transactions are made online and in real time, so that customer and correspondent balances are updated at the same time the transaction is made. Likewise, correspondents issue receipts showing specific details about every transaction carried out.

This initiative is beneficial for the three parties involved: customers achieve convenience, CREDICAMPO retains customers, and correspondents get greater visitor traffic, meaning more potential customers. It is worth mentioning that this service does not translate into additional cost for customers as the commission for each transaction is borne by CREDICAMPO.

In March 2021, 179 CREDICAMPO customers made payments through this network; as of September 2021, the figure had grown to 2,972 customers, with numbers expected to increase every month.

SUMA FINANCIERA IN PANAMA IMPROVES CUSTOMERS' RESILIENCE CAPABILITIES

SUMA Financiera in Panama has a broad product and service portfolio supporting the development cycle of both businesses and owner families.

As of December 2020, SUMA Financiera had 2,967 customers, 42% of which were women and 8% in the agricultural sector. SUMA Financiera identified the fragility of its segment of rural producers, as they are exposed to the effects of climate change such as long consecutive periods of drought in the country’s livestock production areas thus affecting producers.

In view of this vulnerability, SUMA Financiera launched in 2021 the product "SUMA Productor" providing environmentally sustainable financing to livestock producers. This is an alternative for livestock producers, allowing them to increase the profitability of their activity through better use of productive assets; this includes the reduction of the producer’s vulnerability and environmental impact by introducing as added value adaptation and mitigation practices for climate change, plus the financing that generates liquidity for the steady development of the activity.

23 clients have been financed to date who, in addition to a fair interest rate, receive training through a curriculum designed to this end. The topics covered in the course are: environmental efficiency; technology and equipment; sanitary management, sanitation, excreta management; water treatment; reproduction, genetics, among others.

BANCO ADOPEM IN THE DOMINICAN REPUBLIC FINANCES AND PROMOTES GREEN HOMES

The Adopem Savings and Credit Bank, through its innovation process recognized by international entities such as the Inter-American Development Bank (IDB) and the CODESPA Foundation, identified the need to support the transformation of housing conditions and access to quality basic services for low-income populations in rural areas of the Dominican Republic. To date, 35% per cent of the rural population has no access to quality drinking water on a consistent basis.

As of December 2020, Banco Adopem served 163,771 clients, out of which 66% were women and 67% in the rural sector. This perspective was influential in the Institution’s change from the concept of rural housing to that of rural habitat, addressing the needs for improvement in issues such as use of space, lack of ventilation, insufficient lighting and type of construction.

In order to improve the quality of life of its customers and the environment in which they live, Banco Adopem designed a new financial product including a comprehensive approach, Eco Vivienda Adopem, with three purposes: i) investments in water and sanitation (bathrooms, showers, toilets, water filters, biodigesters, etc.); ii) energy and lighting (use of solar panels); iii) infrastructure and livelihood (expansion of housing, improvement of construction areas, etc.).

In order to promote the product, interest rate incentives were established plus a package combining a loan for water and sanitation with working capital. In addition, alliances were developed with recognized international organizations for the promotion of access to drinking water and sanitary conditions for the poorest, thus enabling to target geographical areas, clients and types of potential uses. The alliances were helpful in the setting-up of a curriculum plan for the training and awareness-raising of Adopem's field and managerial staff in the topics like water and sanitation, ecological housing, and renewable energy, among others. As of September, 64 families have been financed with this product.

PILLAR 2 - Using digital technologies to improve operations in MFIs

FINSOL IN HONDURAS STRENGTHENS ITS INTERNAL PROCESSES

In recent months FINSOL Honduras has adopted important changes to its internal processes, in order to provide its staff with efficient and high productivity tools translating into better customer service through new technological solutions.

This was the vision that helped FINSOL implement the Mobile Digital Agenda, an application designed to streamline the field work of loan officers and collections managers, especially to:

- Support field portfolio management.

- Monitor the fieldwork of officers and managers.

- Map customer location.

- Create an environment for applying for a new loan.

- Provide product status information to customers.

Outcomes:

- Faster response time and better customer experience, with loan disbursement time decreasing by at least 1 day in less than 10 months of implementation.

- Officers' work schedule fulfillment improved significantly, from 66% in December 2020 to 97% in September 2021.

- As of September 2021, 87% of customers entered into the Digital Mobile Agenda were geolocated.

- As a result of better loan portfolio management, quality has improved steadily every quarter with PAR 30 decreasing 6% from March 2021 to September 2021.